Usage once mattered greatly for telecom service provider revenues, as most revenue (and most of the profit) was generated by products billed “by the unit.” Lots of things were simpler, back then. Capital investment was fairly easy to model, and profits from incremental investment likewise were easy to predict. All that has changed, as usage (data consumption) of communications networks is not related in a linear way to revenue or profit, all observers will acknowledge. And that fact has huge implications for business models, as virtually all communication networks are recast as video transport and delivery networks, whatever other media types are carried.

Something on the order of 75 percent of total mobile network traffic in 2021, Cisco predicts. Globally, IP video traffic will be 82 percent of all consumer internet traffic by 2021, up from 73 percent in 2016, Cisco also says.

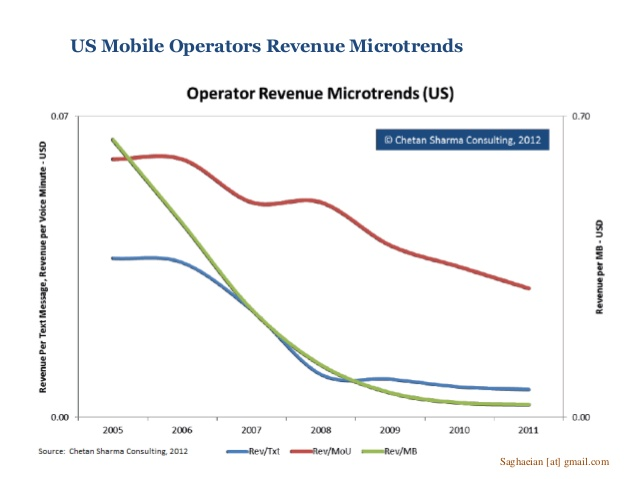

The basic problem is that entertainment video generates the absolute lowest revenue per bit, and entertainment video will dominate usage on all networks. Conversely while all narrowband services generate the highest revenue per bit, the “value” of narrowband services, expressed as retail price per bit, keeps falling, and usage actually is declining, in mature markets.

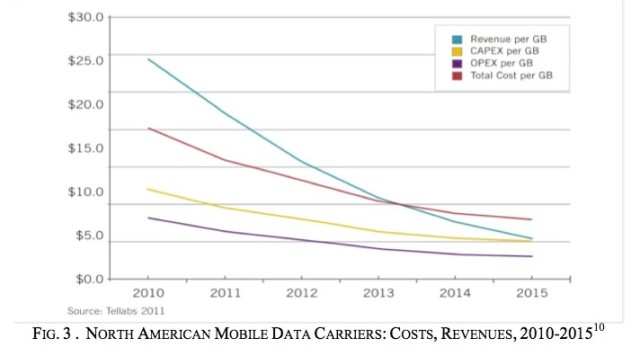

Some even argue that cost per bit exceeds revenue per bit, a long term recipe for failure. That has been cited as a key problem for emerging market mobile providers, where retail prices per megabyte must be quite low, requiring cost per bit levels of perhaps 0.01 cents per megabyte.

Of course, we have to avoid thinking in a linear way. Better technology, new architectures, huge new increases in mobile spectrum, shared spectrum, dynamic use of licensed spectrum and unlicensed spectrum all will change revenue per bit metrics.

Yet others argue that revenue per application now is what counts, not revenue per bit or cost per bit. In other words, as for products sold in a grocery store, each particular product might have a different profit margin on sales, and what matters really is overall sales, and overall profit levels, not the specific profit levels of products sold.

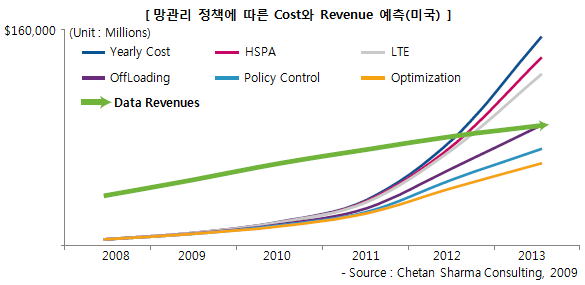

So the basic business problem for network service providers is that their networks now must be built to support low revenue per bit services. That has key implications for the amount of capital that can be spent on networks to support the expected number of customers, average revenue per account and the amount of stranded assets.

Operating costs also become a continuing issue, as the cost per customer is high and getting higher, as competition shrinks the market share any proficient provider can expect to obtain.

As always, the problem is that propensity to spend is fairly linear, while data consumption and demand are non-linear. So the solution to maintaining a revenue-cost relationship that is positive is to reduce the cost of supplying a bit, add new revenue sources higher in the stack, add new geographies and accounts or otherwise gain scale.

Not many who were in the communications business 50 years ago would have believed that would be the case, and so dramatically necessary.