Competition in the Italian mobile market, especially from new entrants who need more spectrum, seems to be driving up 3.6 GHz to 3.8 GHz spectrum prices, which are now being auctioned in Italy. That can be a big problem, as industry executives with long memories can attest. In the past, 3G auction prices were bid up so high they nearly bankrupted the winners.

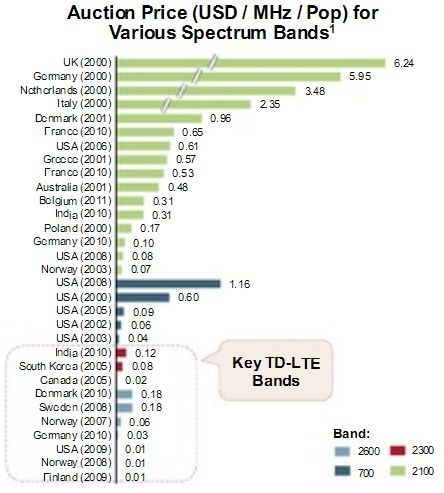

Generally speaking, spectrum prices on a potential user basis have been declining since 2000.

But heightened competition in the Italian mobile market, with new contestants needing lots of new spectrum, seems to be driving prices higher in the auctions for spectrum in the 3.6 GHx to 3.8 GHz band to be used there for 5G networks.

In one way, mobile competition eased when mobile operators 3 Italia and Wind Telecomunicazioni merged and form Wind Tre, reducing the number of competitors, which also include Vodafone, Telecom Italia.

On the other hand, Iliad is making a big push in Italy, while fixed network provider Fastweb is entering the mobile market for the first time. So it appears the new competitors, in need of lots of new spectrum, are forcing prices higher.

Italy’s 5G auction already has crossed the €5.2 billion ($6.1 billion) threshold, about double what the Italian government had originally expected to make.

The 700 MHz auction, just ended, raised more than €2 billion ($2.4 billion).

In other countries, spectrum prices should continue to fall.

The amount of new wireless and 5G spectrum coming to market in the United States and other countries is staggering and beyond anything we have seen in the history of communications. Consider that all mobile operators in any single country have access to about 600 MHz to 1300 MHz of total bandwidth available.

In the 5G era, as millimeter wave spectrum is released, raw bandwidth will increase by up to 1.5 orders of magnitude in physical terms, in many markets. Unlicensed bandwidth alone might grow by about five times to 12 times, compared to available mobile spectrum.

And that will have huge price and capability implications. For the first time, mobile substitution, on a basis comparable with fixed networks, should be possible Access to all that new bandwidth will mean the mobile network’s cost per bit and retail cost, plus usage allowances, should be equivalent to, or perhaps better than, fixed network alternatives.

If you though mobile substitution was a problem for fixed networks when confronted by mobile telephony, consider what might happen next as mobile networks become a full substitute for fixed network internet access

But “raw bandwidth” is only part of the story. Since millimeter wave networks will require small cells, physical reuse of spectrum will add to the capacity increases. All together, it is possible that bandwidth could grow by up to two orders of magnitude (100 times) in some locations.

And all that is going to cause a reset of business models for both mobile and fixed network service providers. Still, in some specific instances, such as Italy, spectrum prices might be a tougher issue.

On the other hand, as spectrum is the price of entry, new entrants and incumbents might conclude they have little option but to spend what is necessary to get 5G spectrum.