t is not hard to find skepticism about the size of 5G markets, for good reason. Not every market is equally well disposed to generate new revenue sources, at scale, and not every set of service providers in every market has the same level of actual need to find those new revenue sources.

That is why virtually everyone expects 5G to become a commercial reality first in just a handful of countries: the United States, Japan, European Union countries and China. Developed nations plus China, in other words. And some might question how fast most EU markets will adopt.

In part, that early deployment pattern is driven by expectations of financial upside from new applications not possible with 4G. GSMA Intelligence also notes some particularities of the U.S. market that also create a fertile environment.

In other words, opportunities might exist to drive aggressive 5G adoption in the U.S. market. GSMA Intelligence notes that U.S. customers have been robust adopters of “digital” services using their mobile devices, ranging from internet-based messaging and social media to entertainment content, as well as using e-commerce.

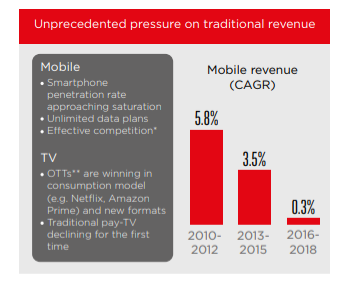

That’s the “pull” of 5G. There also is the “push.” U.S. mobile service revenues have been steadily declining since 2010, and might go negative in 2019. That means the search for additional new revenues is imperative.

So all four leading U.S. mobile operators will be offering 5G mobile services in 2019, with AT&T and Verizon launching mobile 5G services in selected markets in 2018.

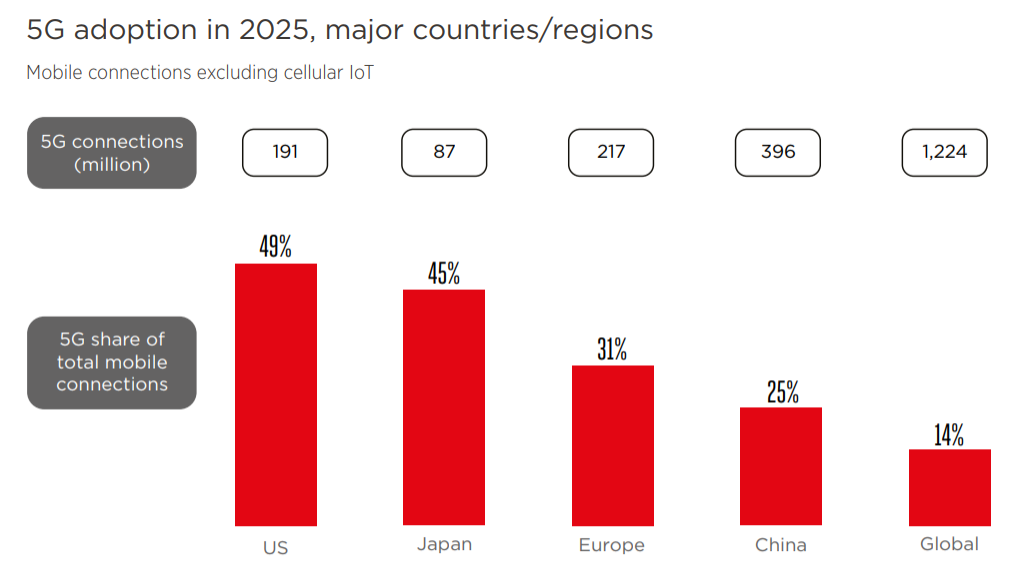

According to GSMA Intelligence forecasts, the United States will experience one of the fastest customer migrations to 5G in the world, with 5G reaching 100 million mobile connections in early 2023. That will make 5G the leading mobile network technology in the United States by 2025, with more than 190 million 5G connections (accounting for around half of total mobile connections), excluding use of 5G to support fixed operations.

But more than supply will drive that deployment speed.

Aggressive millimeter wave spectrum allocations will be key enablers, especially for AT&T and Verizon.

But there are other fundamental reasons for the push into 5G. Simply put, the U.S. mobile market has exhausted its growth model, based on 4G. If one extrapolates from steadily declining revenue growth since 2010, it is possible revenue growth in the core mobile business might actually go negative in 2019.

Since revenue growth is a virtual necessity for firms that are publicly owned, that represents a crisis.

Though new revenue sources will have to be created, 5G offers some opportunity for services that actually have not existed on earlier platforms, including 4G. Though everyone expects early revenue upside to come in the area of “enhanced” (much faster) internet access, that expectation must be qualified.

Since 4G adoption is virtually ubiquitous in the U.S. mobile business, customers who adopt 5G access will, by definition, be replacing primary reliance on 4G. So there is substitution going on, replacing 4G accounts with 5G.

There may or may not be incremental upside from such substitution. In the early days, some incremental upside is likely.

Longer term, the hope is that brand new revenue streams can be created in the internet of things (sensor communications) area. There also is hope some new classes of apps can be created in the ultra-low-latency area. Connected cars or 4K and 8K video, plus other latency-dependent apps such as remote surgery come to mind.

The important point is that U.S. mobile operators are going to be aggressive about 5G because the 4G business model has become exhausted.