The advice to “go digital” or “digitally transform” is almost meaningless these days. Firms already use all manner of technologies, ranging from smartphones and PCs to the internet to mobile apps and cloud computing. All information technology, and virtually all communications technology these days, is “digital.”

The point is that “digital” or “digital transformation” might often be confused with “using digital technology.” The implication often is that “digital” increases value. It unquestionably does so for end users and consumers. As a business model issue, though, digital transformation also destroys supplier value, measured in terms of profits suppliers earn when supplying “digital” products to customers or end users.

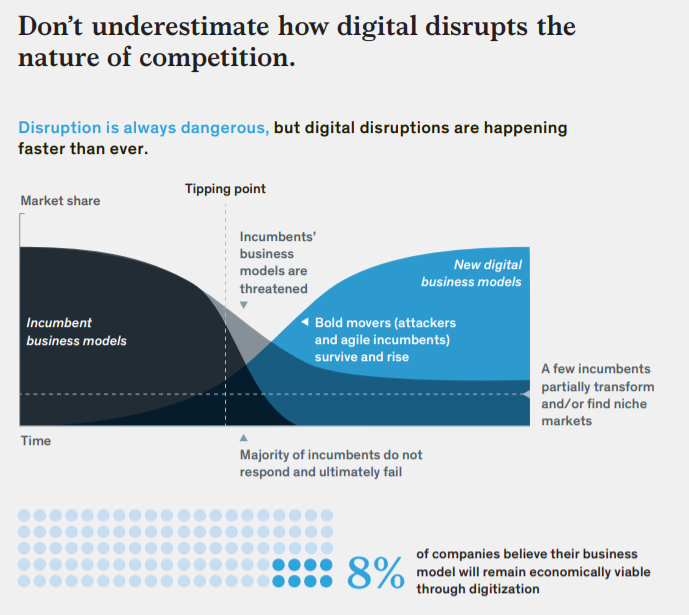

In the internet era, the overlooked observation is that “digital” might actually destroy supplier value, even as it increases end user value. We have seen this process at work in music, publishing, video subscriptions, retailing, the travel bookings business, ride sharing, lodgings and communications.

Once upon a time, the sole lawful provider of “voice service” was one telco in each country. At one time the sole providers of mobile “messaging” were mobile operators. In the past, only one supplier could provide “broadband” data access or private wide area networks.

“Digital” has eroded service provider value as the main or sole providers of voice, messaging, private network services or broadband internet access, allowing third parties to supply those values, with diverse business models.

One way of describing this process is to say “digital is destroying economic rent, which is profit earned in excess of a company’s cost of capital.” In other words, digital transformation–intended to help firms improve or save their business models–might often only hasten their demise.

Among the reasons for the danger is that digital processes tend to create more value for customers than for firms, says McKinsey.

The “consumerization of information technology” involved employees bringing their own consumer tools and using them at work. In many cases, the consumer tools were better than the business tools. That also forced suppliers of enterprise IT to essentially compete with lower-cost consumer offers, shrinking markets, revenue and profit margins in the process.

Digital also renders distribution intermediaries obsolete. That process, known as disintermediation, devalues the function of distribution or retail channels.

“Competition of this nature already has siphoned off 40 percent of incumbents’ revenue growth and 25 percent of their growth in earnings before interest and taxes (EBIT), as they cut prices to defend what they still have or redouble their innovation investment in a scramble to catch up,” McKinsey argues.

The lesson is clear enough: digital shifts value within the ecosystem. Companies and industry segments that captured the value that was left often came from a completely different sector than the one where the original value pool had resided.

Also, to the extent that digital economics rely on network effects–and therefore scale–scale providers tend to win disproportionately. And those providers tend to be app providers whose products are consumed over the top on all internet access networks. That is another way value shifts from one industry segment to others.

So what does “digital transformation” really mean for connectivity service providers. On the operational side of the business, more efficient and therefore lower-cost operations are the hope.

On the strategic side of the business–the core business model–digital transformation might be malignant, in the sense of allowing value–and revenue upside–to migrate to other parts of the value chain.

So digital transformation is, at best, a useful operational tool. On a strategic level, the shift to digital arguably destroys value for the connectivity business.

The logical firm responses range from cost cutting to asset divestitures to acquisitions to gain scale to redeploying capital in adjacent and new business roles.

But the notion that digital transformation is universally valuable for connectivity providers arguably is false.