A study by GSMA Intelligence might be useful, in terms of looking at firm sustainability and competition, after the merger or T-Mobile US and Sprint. A key argument in the debate over the merger of T-Mobile US and Sprint was its impact on competition and consumer welfare (prices being the measure).

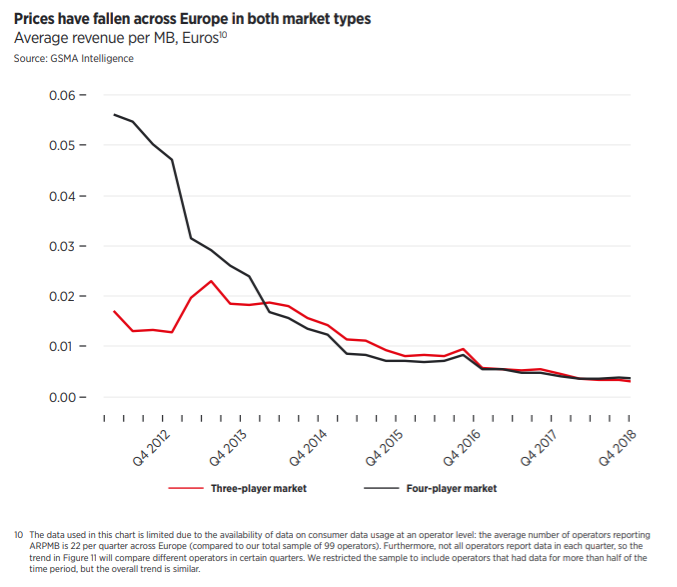

Since 2013, in European markets, average mobile internet prices per megabyte have been the same, in both four-provider and three-provider markets. In other words, it is not clear that three-provider markets lead to higher prices, or that four-provider markets lead to lower prices.

Importantly, the GSMA Intelligence data shows that prices per megabyte started out much higher in four-provider markets, compared to three-provider markets. So something other than competition is involved.

Two trends–arguably unrelated to the number of competitors in a market–have contributed to the reduction in the average revenue per megabyte, GSMA Intelligence suggests. First, prices have simply dropped in all markets, no matter how many providers compete. That will lead some to conclude that, in principle, three competitors are enough to produce consumer welfare gains.

Also, customers simply are buying more data, and that means a volume discount. Average data usage per user has increased 12-fold between 2011 and 2018, GSMA Insight says.

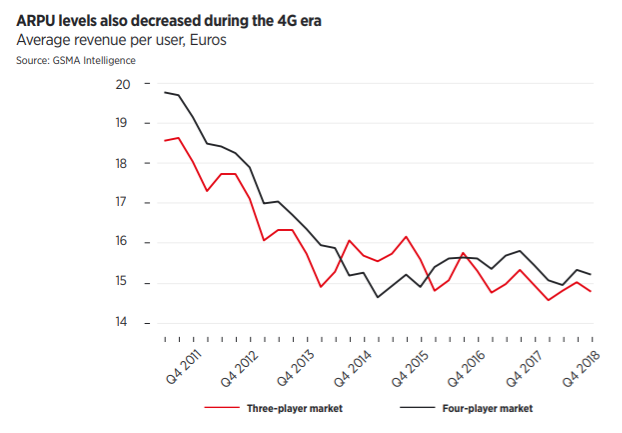

Nor is it clear that the number of service providers affected average revenue per user. In fact, average prices per user were actually higher in the four-provider markets, compared to the three-provider markets, which counter-intuitively is the opposite of what theory would predict.

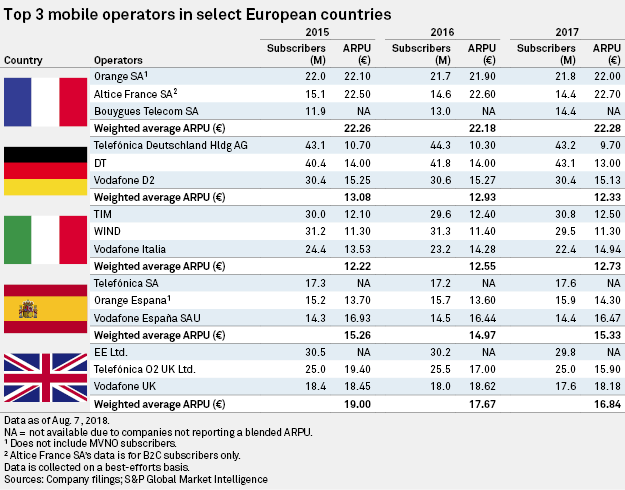

At least in part, that might be driven by other trends. Germany, the strongest economy in Europe, moved from four providers to three. France moved from having three providers to four. Germany has substantially lower ARPU than other countries, for example, and is about half that of France, which moved from three providers to four. So it is possible that most of the change in ARPU is explainable simply by a few countries making moves one way or the other, in terms of number of national contestants.

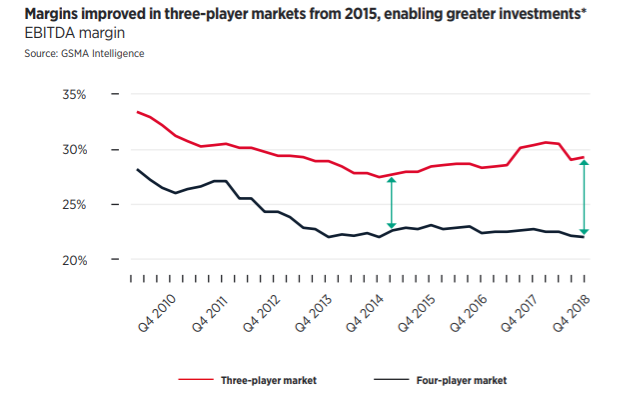

The GSMA Intelligence study suggests it is likely that profit margins will be higher for the three remaining national leaders, as profit margins in European “three-provider” markets have been consistently higher than in “four-provider” markets.

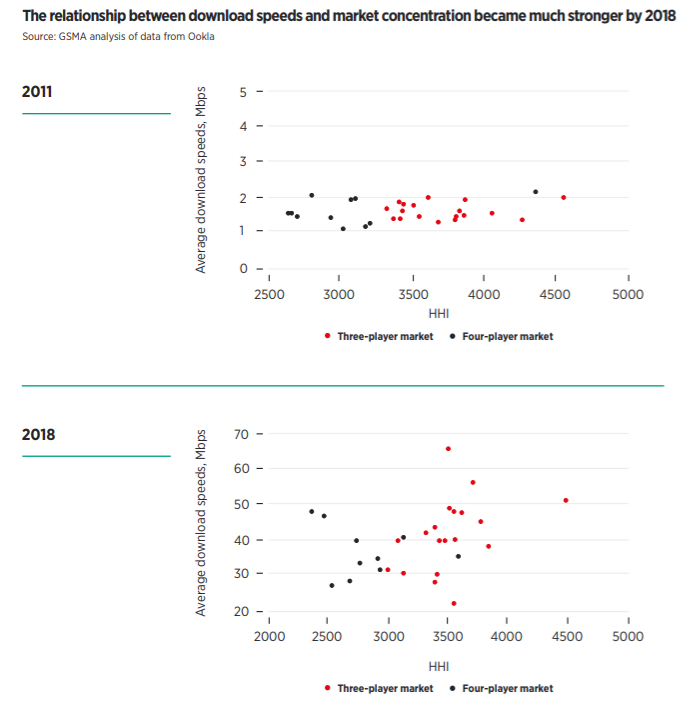

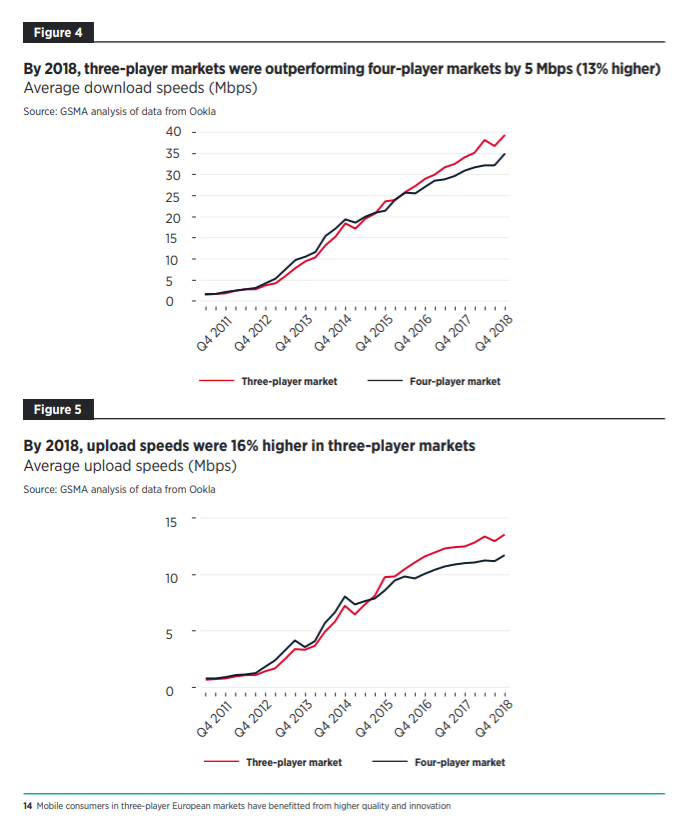

At the same time, there is evidence that three-provider markets were able to produce faster internet access speeds than in four-provider markets, which might support the thesis that higher profitability did lead to higher investment.

Although some of these developments match what one would expect: namely higher investment in countries where profit margins are higher, the data on prices are inconclusive. Post-merger, should these patterns hold, T-Mobile investment should increase. AT&T and Verizon might, or might not, increase capex spending.

But price trends are harder to predict, based on the European data. Data ARPU might not change much, from the four-supplier market.