Growth now is the key strategic issue in the global telecom business, even in the mobility segment that has driven revenue growth for decades. And there are several dimensions.

For a business that has been driven by “connecting more people” in emerging markets, growth prospects will shift to “higher average revenue per account,” as the number of unconnected people reaches low levels. In other words, mobile service providers will have to sell greater quantities of existing products (more gigabytes of data, principally), or higher-value versions of existing products (faster speeds, bigger usage allowances, higher quality or higher value).

As revenue per unit sold continues to drop, and as new account growth stalls, service providers will have to wring more revenue out of existing accounts.

In many ways, the shift to 5G from 4G is a reflection of that basic problem, as in many markets, most potential customers who want 4G and its features already buy it. So 5G offers a chance to reset and change value drivers. Just as important, 5G offers a chance to create new types of services the 4G network cannot support as well.

Ultra-low latency services and other internet of things use cases are prime examples.

Also, service providers generally have to replace half the revenue they currently own about every decade. If new accounts cannot drive that replacement, then some combination of higher usage and brand-new revenue sources has to be relied upon.

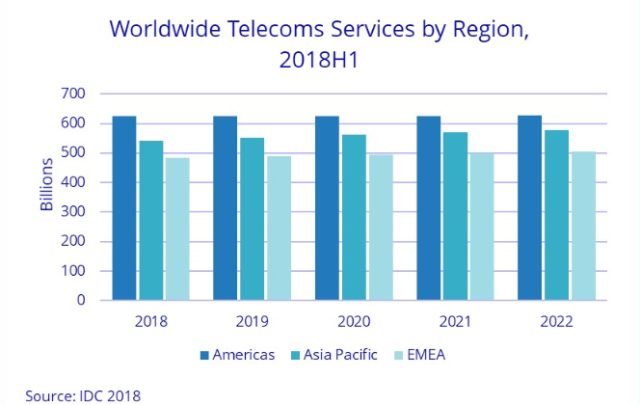

On a non-inflation-adjusted basis, global telecom services revenue will grow at a compound annual growth rate (CAGR) of 0.8 percent, IDC researchers now predict. In any market with inflation rates of at least 0.8 percent, actual revenue will decline.

Product segments within the industry can have faster or slower growth rates. In fact, revenue earned in the fixed network segment generated by data services will grow 22 percent in 2018 and at a four-percent CAGR through 2022, IDC predicts, driven by uptake of internet access services.

Mobile revenue will grow at 1.2 percent through 2022, but fixed network voice revenues will decline at five percent annually to 2022.

“Developed and mature markets will only show marginal gains now, driven by technology migration and bandwidth needs,” said Eric Owen, IDC group vice president, EMEA Telecommunications & Networking. South Asia and Africa are the two regions that will see the fastest revenue growth, IDC predicts.