Just how big a revenue driver mobile video will be for mobile operators in the 5G era is an open question.

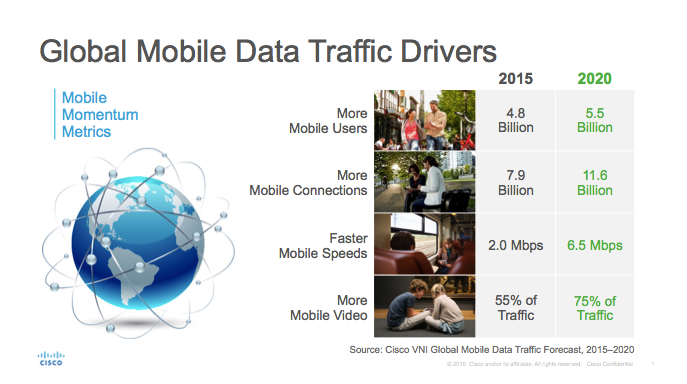

That video will drive mobile data consumption seems not to be contentious. By perhaps 2024, 75 percent of mobile data consumption will be video, most would agree. Of course, consumption and revenue for various participants in the ecosystem is not the same thing.

Connectivity providers learned long ago that though a symbiotic relationship exists between demand for use of internet apps creates demand for internet access services, there is no necessary and direct relationship between use of the internet and revenue generated by provided connectivity.

Quite the reverse, in fact, is most often the case: supply has to be increased without incremental revenue being earned.

Still, many service providers have found that the most-tangible new sources of significant present revenue–troublesome as growth trends might be–come from video subscription services. There simply are not many new revenue sources capable of generating $1 billion or more in incremental revenue for any tier-one service provider.

The problems are compounded for suppliers of fixed-network communications, as voice revenues are falling, while in most developing nations, internet access is slow growing, as nearly all the growth of internet access occurs on the mobile networks.

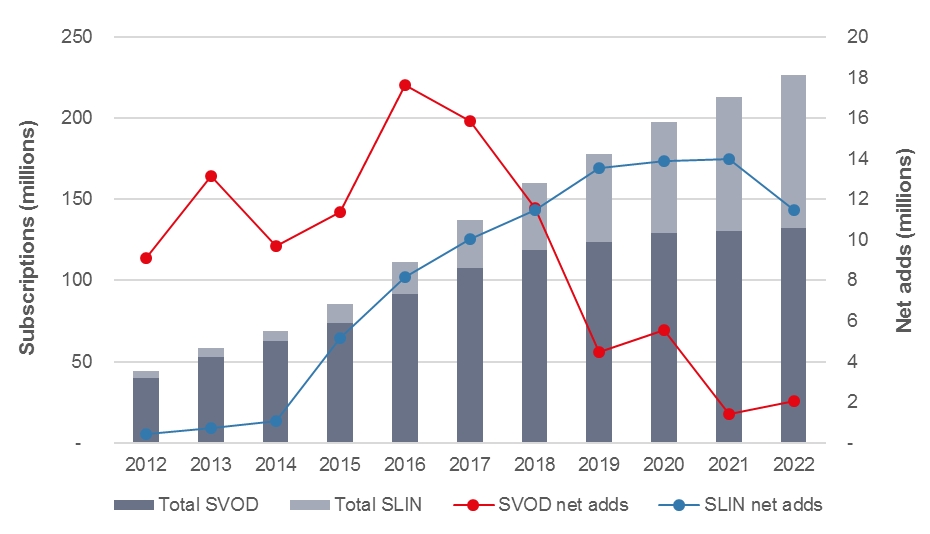

As Ovum analysts have outlined it, linear (SLIN) and on-demand (SVOD) accounts continue to grow, even if there are gross revenue and profit margin implications from faster SVOD growth.

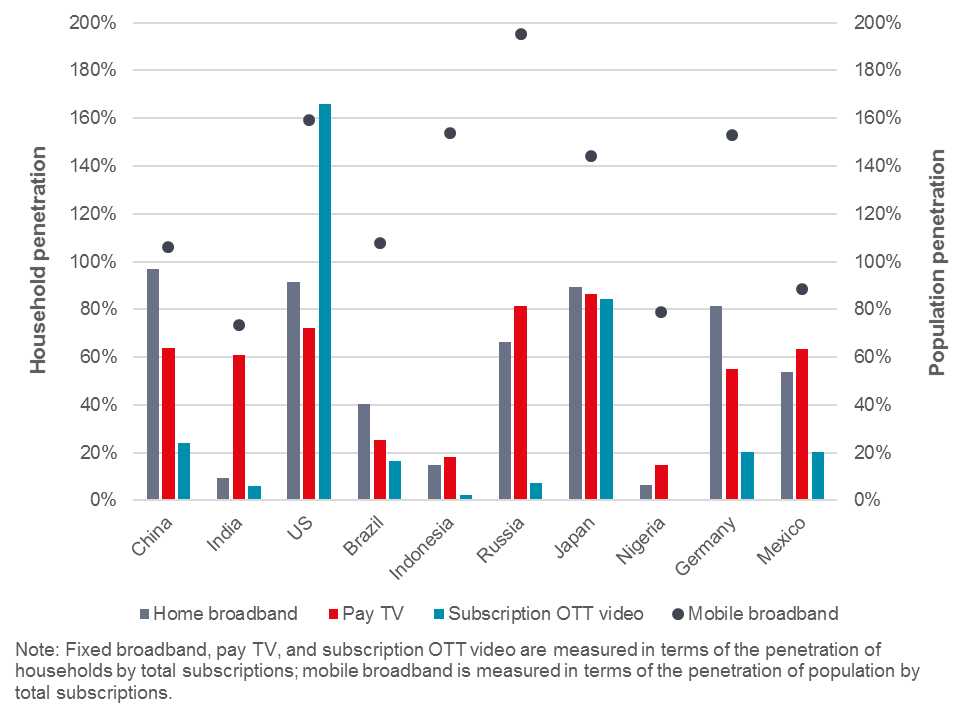

As this graph indicates, in developed nations, fixed internet access is saturated, or nearly saturated, implying slow future growth. Mobile broadband is reaching high levels in developed and now even in some developing markets.

Also, though it would seem that subscription video is fairly well adopted in many markets, total market statistics can mask the market share held by different suppliers. In some markets, most of the video share is gotten by cable TV operators, not telcos.

So where video is a big revenue stream, and mostly earned by cable TV, telcos can grow their own revenues by taking market share, as cable TV operators were able to grow in saturated voice markets or business services by taking share from telcos.

The bottom line is that there are few “new” revenue streams as immediately large as subscription video (both linear and fixed) that have mass market demand and drive subscription or advertising revenue at high levels.

So though much remains to be seen, prospects for mobile subscription video, given the significant and growing consumption of video on mobile devices, is an obvious place to look for future growth.