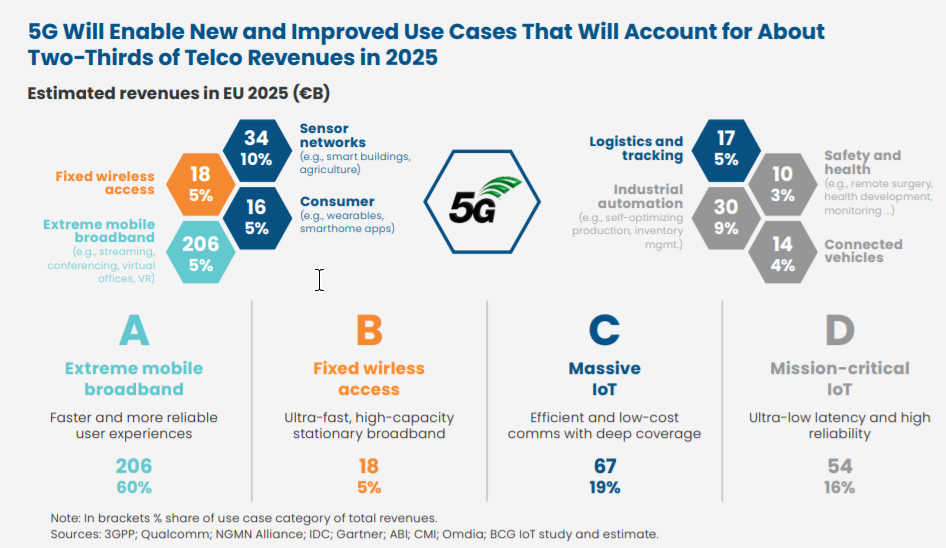

A new report issued by the by BCG for the European Telecommunications Network Operators’ Association suggests new use cases enabled by 5G will generate nearly 66 percent of total “telco” revenues by 2025.

That seems unrealistic in the extreme. For starters, mobility services in Europe account for about half of total revenues. Were 5G to displace 100 percent of telecom revenues, 5G would account for about half of total revenues, best case.

Even the more-focused argument that 5G might drive 66 percent of “mobile revenues” by 2025 is plausible only if one assumes that 5G replaces most existing mobile revenue and adds substantial new fixed wireless, internet of things revenue, despite the existence of competing networks and use of premises wireless that does not necessarily create substantially higher connectivity revenues.

Do you really believe IoT drives 35 percent of total mobile revenue by 2025? Were that the case, do you not believe revenue forecasts would incorporate that expectation? Of course, there is a rational explanation.

Legacy telecom revenues could drop so much that new IoT revenues simply allow the industry to tread water. The larger problem is that the typical firm in the telecom industry has to expect to lose about half its current revenue about every 10 years.

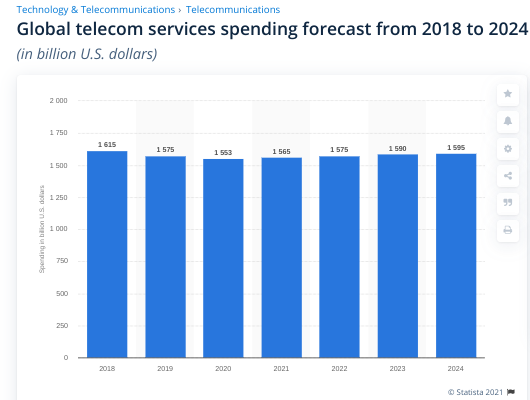

That means the mobile industry has to expect to replace about $500 billion in recurring revenue, while fixed network operators have to expect to replace $400 billion in recurring revenues, within 10 years, assuming global revenues in the $1.8 trillion range by perhaps 2025.

Those are daunting numbers.

In Asia and much of the Pacific, mobile revenues account for something closer to 70 percent of total revenue. In the Middle East, mobile revenues account for as much as 80 percent of total revenue. In such regions, one might argue that the impact of incremental new IoT revenues could be substantial.

But that remains a tall order. GSMA has estimated service provider IoT connectivity revenue at less than $45 billion globally by 2025. In a global business of $1.6 billion, IoT at that level would represent less than three percent of total industry revenues, but possibly six percent of mobile revenues.

That the report is issued at all reflects the importance communications regulators have in creating and shaping the business model. It is deemed necessary, from time to time, to “remind” regulators and politicians of the economic contributions an industry makes.

In that regard, the ETNO report argues that 5G and gigabit fixed networks can provide enormous economic benefits. No surprise there. What would be surprising is an argument that no financial help is required and that 5G is such a lucrative thing that service providers cannot wait to deploy it.