With the exception of markets in Asia, Africa or elsewhere that still are adding subscriber accounts and mobile data accounts, developed markets where 5G is first deployed will not likely see too much of an upsurge in revenue, for several reasons.

To start, 5G will not be available in many markets, to begin with. And in markets where 5G is available, where mostly everyone who wants to buy mobile service already does so, 5G accounts will simply cannibalize 4G accounts. So if one assumes there is a modest cost premium for 5G, incremental revenue is likely to be relatively subdued.

For such reasons, “there is limited growth left in connectivity revenue for service providers,” Strategy Analytics says.

In fact, Strategy Analytics predicts mobile service revenue will peak in 2021 at US$881 billion, just three percent above the level forecast for 2018.

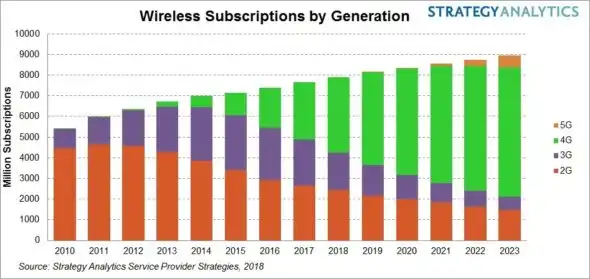

User-linked mobile 5G connections will grow from 5 million in 2019 to 577 million in 2023 (excluding fixed wireless applications and industrial IOT). These will account for 10 percent of connectivity revenue in 2023.

That maturation of the mobile market is why 5G revenues earned from human customers will be very slight. Each new 5G account cannibalized an existing 4G account, so net revenue gains are limited to the difference between a typical 5G account revenue and typical 4G account revenue.