Industry competitors normally pay money to track their market share versus their “real” competitors. The problem is that, in rapidly-changing and porous new markets, the legacy competitors–even when they are the most benchmarked firms–are not the strategic competitors.

These days, many service providers would say that “Google” or other app providers are their key competitors, even as they continue to benchmark against others in their “narrow” markets (mobile market share, or fixed network video or internet access).

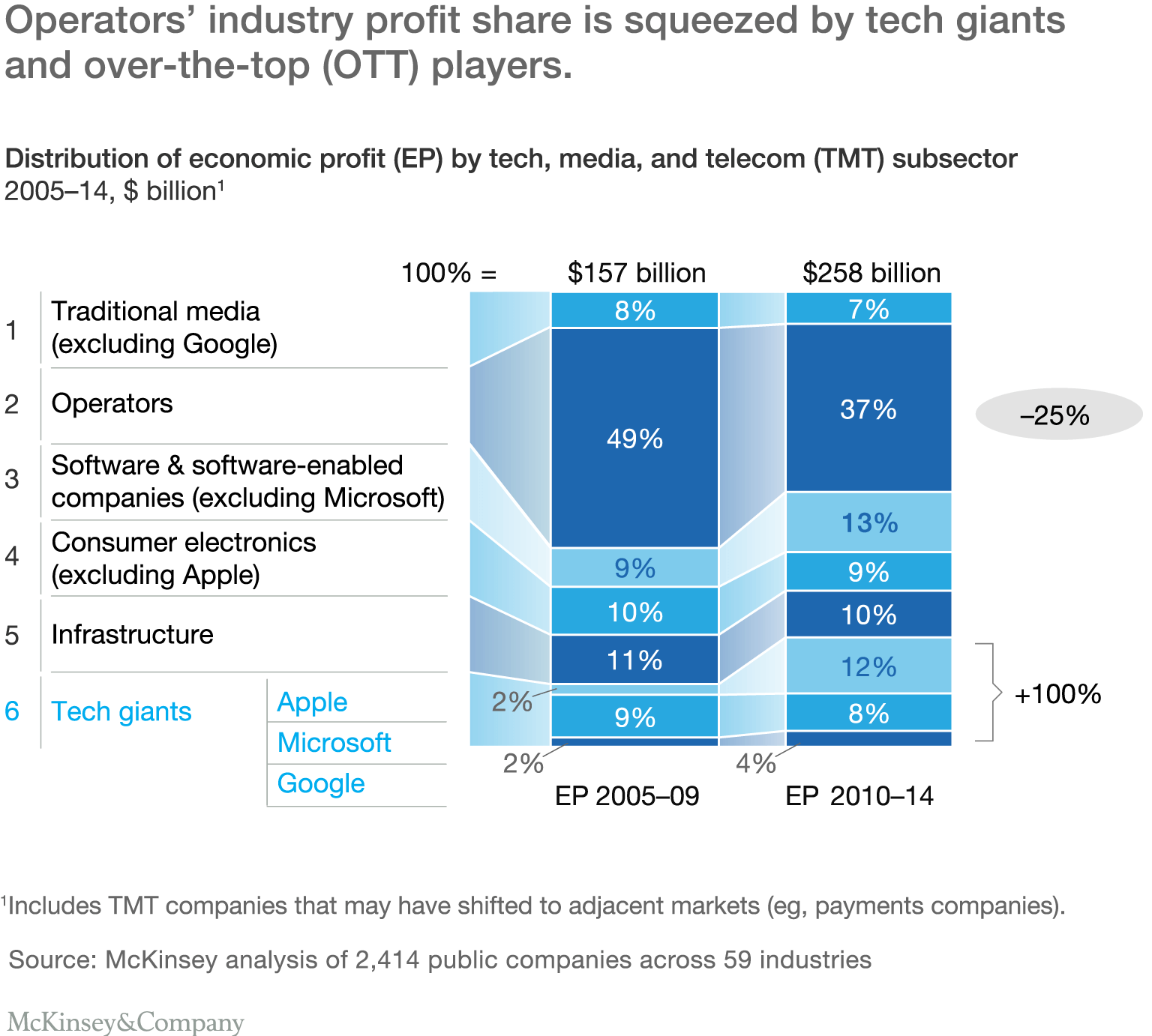

The biggest single change in the internet value chain between 2005 and 2010, for example, was the shift of revenue from telcos to Apple, Microsoft and Google. Telecom providers lost 12 percent of profit, while Apple, Microsoft and Google gained 11 percent.

Nevertheless, the strategic issue is diminishing relevance. The “access to the internet” and associated service provider functions simply represent less value in the internet ecosystem, compared to apps, devices and platforms.

But sometimes, the traditional “narrow market definition” competitors really contribute to value loss.

In any ecosystem, one segment’s revenue is another segment’s cost. So when Reliance Jio says it saved consumers $10 billion in a single year, that also means the mobile and telecom industry lost $10 billion in annual revenue.

You would be hard pressed to name any single other competitor that has had that immediate impact and value destruction, in a single year.

You might say that is an example of Reliance Jio literally destroying the older telecom model and recreating it with new leadership and price points.

Tactically, Reliance Jio (a traditional competitor in the mobile or telecom market) has had the greatest impact. Strategically, app, device or platform providers will erode the most value, longer term.